Get the latest on coronavirus. Sign up to the Daily Brief for news, explainers, how-tos, opinion and more.

No one likes being in debt. The dark cloud of money owed to others has hung over most of us at one time or another, and getting out from under its shadow normally involves discipline, graft and a depressing lack of fun stuff.

But what about when that dark cloud is hanging over a government?

Largely as a result of the coronavirus pandemic, it’s been estimated the UK will have to borrow nearly £300bn this year, a sum so vast it’s pretty incomprehensible.

And at some point, the government – and in turn we – will have to pay it back.

Sounds grim – do we have any other options?

Unfortunately not. One person who knows quite a bit about the British economy at times of crisis is Lord Alastair Darling, Labour’s chancellor during the financial crash of 2008.

“We just have to accept this is an extraordinary event – we’ve never seen anything like it before in modern times and it’s going to take a long time to recover,” he told HuffPost UK.

“The priority is actually making sure we’ve got an economy when we come through the other side of it.”

Fair enough. Where’s this debt coming from?

As Lord Darling alludes to, the government has made a number of decisions aimed at ensuring that, once we make it through the coronavirus crisis, we still actually have an economy.

One of the costliest interventions is the furlough scheme which sees the government pay a sizeable chunk of wages to those who are temporarily unable to work because of the lockdown.

“You need to keep as many businesses going as possible,” says Lord Darling.

“You need to keep people in work as far as you possibly can so that, when things get better, we can get growing again rather than looking around a completely shattered landscape.”

Where is the government getting this money from?

If you are a bit short on cash, you might ask a mate for a tenner to tide you over until payday. If they’re nice they’ll say yes and if they’re decent to boot, they won’t expect anything in return aside from their original £10 outlay.

If you’re a government it’s a bit trickier. Your “mates” are other governments and it’s unlikely they’ll lend you some money without expecting something in return, which could entail any number of things in the cutthroat and often shady world of geopolitics.

Also, there’s the not-so-small matter of government debts being quite a bit larger than £10 – see above.

So what they do is issue bonds. Someone – usually a large financial institution such as a bank or a pension fund – then buys that bond.

This gives the government some cash to spend and in return, the buyer gets a set amount of money as interest – usually every six months – plus a payout when the bond matures.

Bonds are issued over set time limits – anything from one month to 30-plus years. The longer the bond, the more money the buyer can expect as their investment is being tied up for longer and there is more risk of something going wrong.

They’re generally seen as one of the safest investments you can make but the returns are slow and steady and usually far lower than riskier investments like the stock market.

How do they pay it back?

In essence, a government has two options. The first is the closest to how a household would pay off a debt – reduce your spending and try and up your earnings.

For a government this means cutting public services so the money raised through taxes pays off the debt.

Sound familiar? That’s because it was the preferred method of the Conservatives (and for a while their Lib Dem partners) when they took power in 2010 – AKA “austerity”.

But a government has another option – grow the economy, generate taxes and hope this creates more money than the interest rate on the debt.

Ricardo Reis, professor of economics at LSE, uses the analogy of a student loan to explain how this works.

“When you were 18 you maybe borrowed some money. At that time your income was ridiculously low, but by now your income is much higher.

“Therefore it makes perfect sense to borrow when you were 18 and pay a fraction of what your income is now.”

And bingo – it’s taken quite a few years but you’ve paid off your debt and because your earnings have increased, you’ve barely felt that little wedge of cash coming out of your payslip each week.

How long are we talking?

It’s too early to say but and the scale of the coronavirus crisis isn’t yet totally clear. The last financial crisis in 2008 took around 18 months to recover from, but according to Lord Darling, this isn’t a helpful comparison.

“Yes, there are similarities but this is much, much worse,” he says.

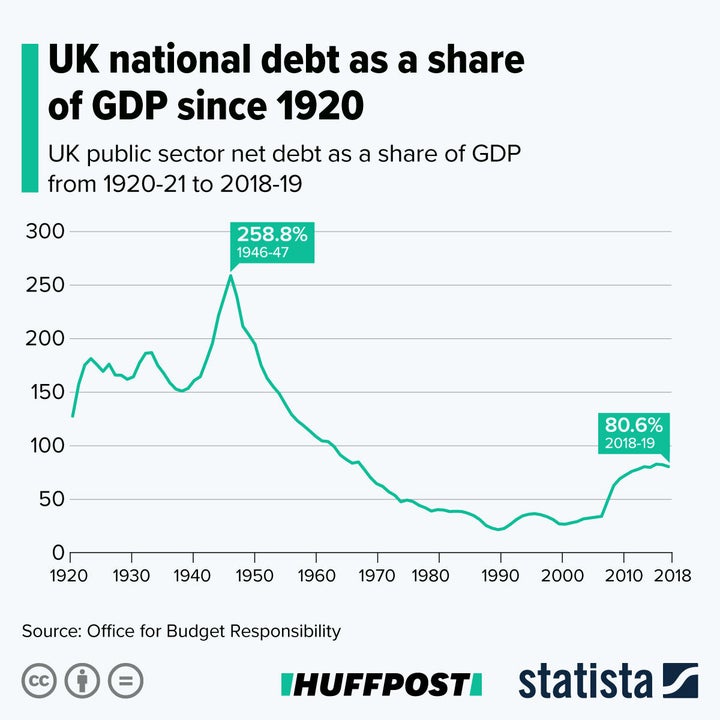

“If you’re looking at debt levels, the better comparison is with what the position was at the end of the second Second World War and if you look at the debts we then, it took decades to pay it off – not until the beginning of this century.”

Which option will the government go for?

It’s too early to say for sure and the fact remains that we don’t even know how big the debt will be or when we could start paying it back.

Last month Boris Johnson ruled out using austerity measures as part of the government’s response to the economic damage caused by coronavirus.

Instead, the prime minister suggested he would plough on with plans to ramp up government spending, suggesting it could “encourage” the economy to “bounce back” after the crisis.

But the PM may clash with the current chancellor, Rishi Sunak. A Treasury document drawn up for the chancellor and dated May 5 said measures including income tax hikes, a two-year public sector pay freeze and the end of the triple lock on pensions may be required to fund the debt.

This has caused a huge outcry. Chair of the Police Federation of England and Wales John Apter called any such move “morally bankrupt” and urged the government to rethink any plans for “financially punishing our public sector workers”.

Infographic supplied by Statista

Calling all HuffPost superfans!

Sign up for membership to become a founding member and help shape HuffPost’s next chapter

Credit: Source link